A Comprehensive Guide to the Weighted Mean Absolute Percentage Error (WMAPE) in Python

Related Articles: A Comprehensive Guide to the Weighted Mean Absolute Percentage Error (WMAPE) in Python

Introduction

With great pleasure, we will explore the intriguing topic related to A Comprehensive Guide to the Weighted Mean Absolute Percentage Error (WMAPE) in Python. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

- 1 Related Articles: A Comprehensive Guide to the Weighted Mean Absolute Percentage Error (WMAPE) in Python

- 2 Introduction

- 3 A Comprehensive Guide to the Weighted Mean Absolute Percentage Error (WMAPE) in Python

- 3.1 Understanding WMAPE: A Measure of Forecasting Accuracy

- 3.1.1 Calculation of WMAPE

- 3.2 Advantages of WMAPE

- 3.3 Limitations of WMAPE

- 3.4 Practical Applications of WMAPE in Python

- 3.4.2 Implementing WMAPE in Python

- 3.5 FAQs about WMAPE

- 3.6 Tips for Using WMAPE Effectively

- 3.7 Conclusion

- 4 Closure

A Comprehensive Guide to the Weighted Mean Absolute Percentage Error (WMAPE) in Python

The Weighted Mean Absolute Percentage Error (WMAPE) is a crucial metric in evaluating the performance of forecasting models, particularly when dealing with time series data. It provides a robust measure of the average percentage error, taking into account the relative importance of different data points. This article delves into the intricacies of WMAPE, explaining its calculation, advantages, limitations, and practical applications in Python.

Understanding WMAPE: A Measure of Forecasting Accuracy

The WMAPE metric is a weighted average of the absolute percentage errors (MAPE) across all data points. It assigns weights to each data point based on its significance, allowing for a more nuanced assessment of model performance. In essence, it measures the average percentage difference between predicted and actual values, considering the relative importance of each observation.

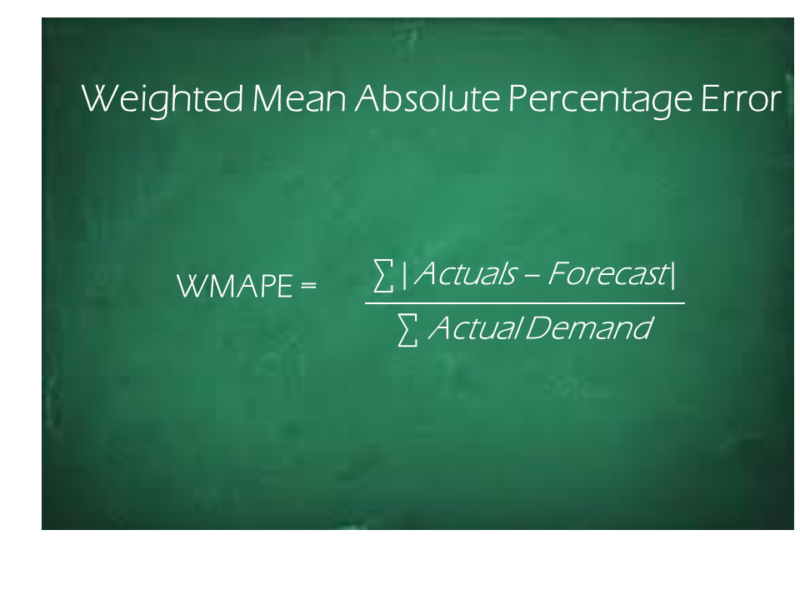

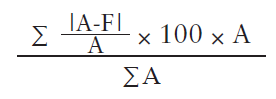

Calculation of WMAPE

The formula for WMAPE is as follows:

WMAPE = (∑(wi * |(Yi - Fi) / Yi|) / ∑wi) * 100Where:

- Yi: Actual value of the i-th data point

- Fi: Forecasted value of the i-th data point

- wi: Weight assigned to the i-th data point

The weights (wi) can be determined based on various factors, such as the importance of specific data points, the volume of transactions, or the time period associated with each observation.

Advantages of WMAPE

The WMAPE metric offers several advantages over other error metrics, making it a valuable tool for evaluating forecasting models:

- Handles Outliers: WMAPE is less sensitive to outliers compared to the standard MAPE, as it weighs the errors proportionally to the importance of each data point. This makes it a more robust metric for datasets with extreme values.

- Reflects Importance: By incorporating weights, WMAPE provides a more accurate representation of model performance, considering the relative significance of different data points. This is particularly useful in scenarios where certain observations hold more weight than others.

- Interpretable Results: WMAPE expresses errors as percentages, making it easy to interpret and communicate the accuracy of forecasting models to stakeholders.

Limitations of WMAPE

While WMAPE offers numerous advantages, it also has some limitations:

- Weight Selection: Choosing appropriate weights can be challenging and subjective. The selection process should be based on a thorough understanding of the data and the specific requirements of the forecasting task.

- Zero Values: WMAPE is undefined when the actual value (Yi) is zero. This can be problematic in datasets with zero values, requiring careful consideration or alternative metrics.

- Non-Linearity: WMAPE is not a linear function of the errors, making it difficult to directly compare the performance of different models based solely on WMAPE values.

Practical Applications of WMAPE in Python

The WMAPE metric is widely used in various forecasting applications, including:

- Sales Forecasting: WMAPE can be used to evaluate the accuracy of sales forecasts, considering the importance of different product categories or customer segments.

- Inventory Management: WMAPE helps assess the effectiveness of inventory forecasting models, taking into account the value of different inventory items.

- Financial Forecasting: WMAPE is valuable for evaluating the accuracy of financial forecasts, considering the importance of different revenue streams or expenses.

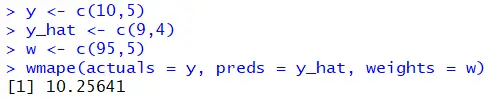

Implementing WMAPE in Python

Python offers several libraries that facilitate the calculation of WMAPE, including:

-

Scikit-learn: The

sklearn.metricsmodule provides amean_absolute_percentage_errorfunction that calculates the standard MAPE. To calculate WMAPE, you can modify the function to incorporate weights. -

Statsmodels: The

statsmodels.tsa.apimodule provides tools for time series analysis, including functions for calculating various error metrics, such as MAPE. You can extend these functions to calculate WMAPE. - Custom Functions: You can create your own custom Python function to calculate WMAPE, providing flexibility in defining the weight calculation and applying it to different datasets.

FAQs about WMAPE

Q: What is the difference between WMAPE and MAPE?

A: The key difference is that WMAPE incorporates weights, allowing it to consider the relative importance of different data points. MAPE, on the other hand, treats all data points equally.

Q: How do I choose appropriate weights for WMAPE?

A: The weight selection process depends on the specific application and data characteristics. Factors to consider include the importance of individual data points, the volume of transactions, and the time period associated with each observation.

Q: What are some alternative metrics to WMAPE?

A: Other error metrics include the Mean Absolute Error (MAE), Root Mean Squared Error (RMSE), and Symmetric Mean Absolute Percentage Error (SMAPE). The choice of metric depends on the specific requirements of the forecasting task.

Q: Can WMAPE be used for non-time series data?

A: Yes, WMAPE can be applied to non-time series data as well, as long as the data points have associated weights. However, it is particularly useful for time series data where the importance of different data points may vary over time.

Tips for Using WMAPE Effectively

- Understand your data: Before applying WMAPE, thoroughly understand the data and the significance of different data points.

- Choose appropriate weights: Carefully select weights that accurately reflect the relative importance of each data point.

- Consider alternative metrics: Evaluate the performance of your forecasting model using multiple error metrics to gain a comprehensive understanding of its accuracy.

- Interpret the results: Analyze the WMAPE values in context, considering the specific application and the chosen weights.

Conclusion

The Weighted Mean Absolute Percentage Error (WMAPE) is a powerful metric for evaluating the performance of forecasting models, offering a nuanced assessment of accuracy by incorporating weights. Its ability to handle outliers, reflect the importance of different data points, and provide interpretable results makes it a valuable tool for various applications, particularly in time series analysis. By carefully considering its advantages, limitations, and practical implementation, users can leverage WMAPE to enhance the accuracy and reliability of their forecasting models.

Closure

Thus, we hope this article has provided valuable insights into A Comprehensive Guide to the Weighted Mean Absolute Percentage Error (WMAPE) in Python. We appreciate your attention to our article. See you in our next article!